The Noise:

Let’s be real—in India, the monsoon isn’t just a weather report. It practically dictates the entire rural economy. So, when the rains don’t show up on time or dump too much water at once, the whole agricultural supply chain feels the sting.

Lately, there’s been a ton of panic surrounding Dhanuka Agritech Ltd., mostly because of some serious short-term bumps in their earnings for the 2025–2026 fiscal year. Have you looked at their stock lately? It’s taken a massive hit, dropping about 50% from its 52-week high of around ₹1,960 to land somewhere near ₹985 today. The market absolutely hates missed expectations, and it has punished this stock relentlessly.

Here is exactly what triggered the panic:

Earnings Drop: Profit took a 27.33% year-over-year dive in Q3 FY26, landing at ₹40.00 crore. Naturally, investors flinched.

Dialing Back Promises: Management had to swallow their pride, downgrading their hopeful “double-digit” growth forecast to a much more cautious “flattish” outlook.

The Weather Trap: Thanks to those erratic monsoons, they saw an unprecedented amount of unsold goods returned by farmers—roughly ₹220 crore worth in just the first nine months of FY26.

Regulatory Headaches: A sudden government freeze on bio-stimulant sales threw a massive wrench into their day-to-day operations. That sudden stop ended up costing them an estimated ₹49 crore in lost revenue over just nine months in FY26.

The Cost of Growing: They’re pouring over ₹300 crore into a massive new manufacturing plant in Dahej. Right now, it’s dragging down their overall profits because it isn’t making money yet.

The Signal:

When you see a stock chart fall off a cliff, it’s incredibly easy to assume the business is broken forever. But if we tune out the short-term noise, the long-term fundamentals actually look incredibly solid.

What we’re really looking at is a fundamentally strong company going through a massive, deliberate transformation. For decades, Dhanuka made incredible returns by acting as the exclusive Indian distributor for patented Japanese agrochemicals. Now? They’re taking control of their own destiny. They are building their own chemicals at the new Dahej facility and buying up global rights to products—like their recent ₹165 crore deal with Bayer AG.

Their core ability to generate cash is still very much alive. The competitive moat around their business is intact, even if their baseline return on capital is taking a temporary dip while they get these new factories up and running.

Looking Through the Value Investor’s Lens

To figure out if this is a classic “value trap” or a genuine mispricing opportunity, we need to think like business owners. Here’s a quick snapshot of what Dhanuka actually does:

What They Make: Everything from weed killers and bug sprays to plant growth boosters. They have over 300 registered products and actively sell about 90 of them.

Where They Make It: They run four factories across India, including that brand-new, heavy-duty plant in Dahej, Gujarat.

How They Sell It: This is their true superpower. They have an insane network of 6,500 distributors and 80,000 retailers, allowing them to reach roughly 10 million farmers across India.

Global Friends: They partner with big global players (especially in Japan and the US) to bring advanced, patented chemicals to India. And with that recent Bayer deal, they are stepping onto the global stage themselves.

Here is how the business breaks down when we look closely:

1. A Deep, Defensible Moat

Dhanuka’s ability to win in a tough market comes down to two big advantages:

The VIP Pass to Global IP: Instead of spending decades trying to invent new chemicals from scratch, Dhanuka perfected a smarter model. They are the go-to partner for Japanese innovators like Nissan Chemical and Mitsui Chemicals. These exclusive deals make up about half of Dhanuka’s revenue and give them the power to set prices without worrying about cheap knock-offs. Plus, that ₹165 crore Bayer deal I mentioned? That makes them the actual owner of the intellectual property in over 20 countries.

The Last-Mile Network: In India, the best chemical doesn’t win on its own. It wins when it comes with the right advice from a local agronomist right there in the village. Even if a foreign company invents a better product, trying to replicate Dhanuka’s army of 80,000 retailers would take way too much time and money. It’s just easier—and more profitable—for them to partner with Dhanuka.

2. Financial Fortitude (Because Survival Comes First)

You can’t grow your wealth if the business goes under. Luckily, Dhanuka has a fortress of a balance sheet, sitting on over ₹250 crore in cash and liquid investments.

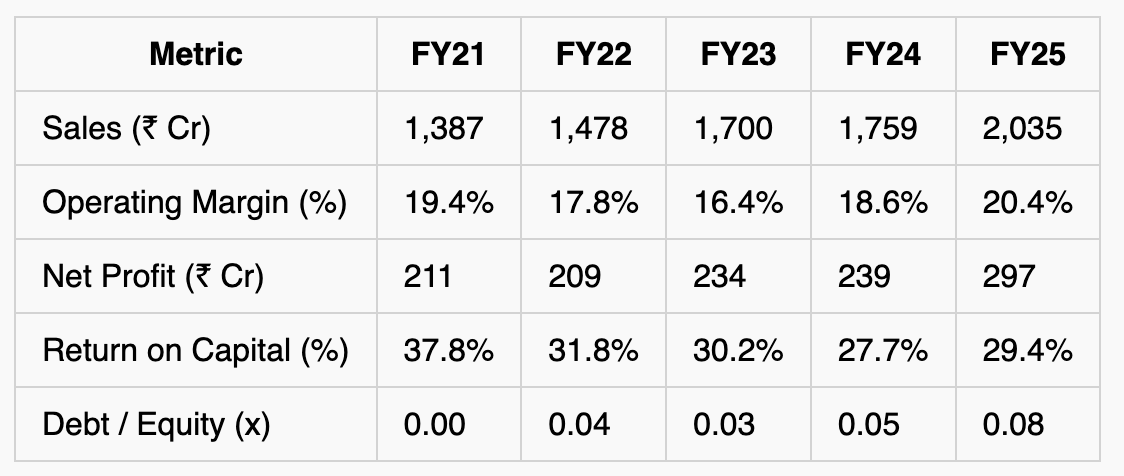

Let’s look at how they’ve performed over the last five years:

What does this actually tell us?

Debt is a Non-Issue: At 0.08x, they basically don’t have any debt. We don’t have to lose sleep over them struggling to pay back loans.

Earnings are Real: The actual cash they bring in consistently matches or beats the profits they report on paper.

Expectations Need to Shift: We have to accept that the glory days of 35%+ returns on capital are probably behind us. As they build and run their own manufacturing, a solid 22% to 25% return is the new, realistic normal.

3. The Governance Check (Looking for Red Flags)

We always want to protect our downside, so we have to look for cracks in the foundation. Being a family-run, mid-sized company, Dhanuka has a few quirks we need to watch:

They loaned ₹15 crore to a lab owned by the founders. That’s a classic red flag when it comes to how they handle our cash.

They tossed ₹30 crore into an unlisted drone startup. That’s a total distraction from their core business, and worse, it’s now tied up in nasty litigation.

There’s a massive ₹121.32 crore tax demand from the government hanging over their heads. We need to keep a very close eye on how that plays out.

4. Valuation: Is it Actually Cheap?

Right now, Dhanuka is trading at a Price-to-Earnings (P/E) ratio of about 16.3x to 16.8x. If we do a little reverse math, the current stock price suggests the market only expects them to grow their free cash flow by a measly 5.2% over the next 10 years.

But historically? They’ve comfortably grown sales and cash flow by 8.5% to 9.3%.

What this tells us is that the stock has a really compelling margin of safety right now. The market is obsessing over today’s bad weather and factory costs, and giving them absolutely zero credit for the future growth that those new Bayer molecules will bring.

5. The Pre-Mortem: How Could We Lose Our Shirts?

Before we buy, we need to figure out what could go wrong. If we look back in five years and realize we lost money on this, it’ll probably be because of one of these three “killers”:

The Dahej Plant Flops: Our whole theory relies on this new plant hitting 80% capacity and turning a profit by FY27. If management struggles to run it, or if China floods the market with dirt-cheap chemicals, Dahej could become a giant money pit.

The Japanese Walk Away: What if global partners like Nissan decide India is finally big enough for them to sell directly to farmers? If they bypass Dhanuka when contracts renew, we lose our high-margin products and get stuck selling cheap commodities.

The Taxman Wins: Remember those tax demands of ₹121.32 crore? If the courts rule against Dhanuka, it won’t bankrupt them, but it will wipe out half a year’s profit, kill any chance of share buybacks, and seriously spook investors.

The Bottom Line

Right now, the market is looking at a painful stretch of bad weather and the temporary costs of building new factories, and confusing it all with a permanent decline. As smart investors, we know that time is the friend of a wonderful business and the enemy of a mediocre one. Enduring a little temporary noise? That’s just the price of admission for creating real, long-term wealth.

Disclaimer: Do your own due diligence before investing.

Join the Hunt.

The market is noisy. Your inbox shouldn’t be.

By subscribing to Budget Tiger, you’re making a commitment to rational, owner-oriented investing. Here is my commitment to you:

One email a week: Delivered every Sunday at 8 AM.

100% Signal: Deep research powered by AI, vetted by human judgment. No spam, no filler.

Always Free.

You’ll get one email a week from me. It will cover:

The Noise: What the AI hype-filter caught (and why to ignore it).

The Signal: The fundamental truth about the cash flows and moats.

The Verdict: A qualitative deep dive, not a quantitative score.

Leave the noise behind. Enter your email below to receive next week’s edition of Budget Tiger in your inbox.