The Noise

It’s easy to get swept away by the roar of the crowd, isn’t it? If you’ve been watching the Indian market over the last four years, you’ve probably heard one deafening story: the unstoppable rise of Defense and Capital Goods. Driven by the very real “China+1” shift and government push, everyday investors have piled in, treating heavy metal manufacturers like the next tech titans.

Meanwhile, the IT sector has been left in the dust. Stock prices have stalled out, and headlines are dominated by fears of global headwinds. If you only look at the stock ticker, you would think Defense is a guaranteed gold mine and IT is a sinking ship.

The Signal

But if we look at businesses like owners, we know the stock ticker is often just a popularity contest. The real truth? It is written in the cash flow.

When we pull back the curtain and look at the fundamental data of companies with over ₹1,000 Cr market cap from April 2022 to April 2026, a completely different picture emerges. The true signal is the massive gap between price action and actual cash generation. While Defense stock prices have surged, their underlying cash flows have quietly evaporated. On the flip side, while IT stock prices have stagnated, their cash-generating engines are running hotter than ever.

The Value Investor’s Lens

Let’s look at the market through the eyes of a business owner across four key sectors:

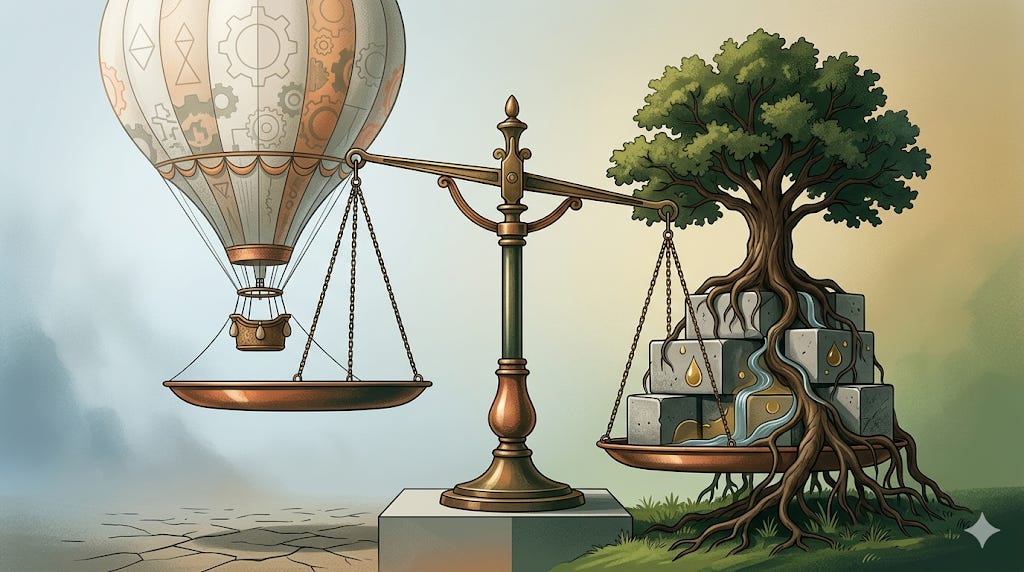

The Illusion of Defense:

Think of a hot air balloon. It expands rapidly and looks incredible from afar, but inside, it is mostly empty air. The defense sector’s median P/E has ballooned from 31 to an eye-watering 56. Yet, the total cash flow from operations actually collapsed from roughly ₹38,500 Cr down to just over ₹15,000 Cr. This is a massive red flag. The 24% price increase is entirely driven by narrative and “multiple expansion” (which is just a fancy way of saying investors are simply willing to pay a higher price for the exact same earnings), not cash-backed value. We need to proceed with extreme caution here.

The Hidden Moat in IT:

If Defense is a fragile balloon, top-tier IT is a deep-rooted oak tree. Despite a 4% drop in price since 2022, the underlying business reality is rock solid. These companies require almost no capital to grow. The sector grew its absolute cash flow from ₹1.19 Lakh Crs to ₹1.52 Lakh Crs, all while maintaining a stable valuation multiple. The market is completely ignoring this cash generation. For patient owners who favor zero debt and high ROCE (Return on Capital Employed—measuring how efficiently a company turns capital into profit), there is real value accumulating right under our noses.

The Banking Cash Machine:

Banks have been doing something right. Armed with their cleanest balance sheets in a decade, strict lending rules, and strong access to cheap Current and Savings Account deposits (CASA), their return on capital bumped up nicely. Cash flows expanded to a massive ₹3.49 Lakh Crs. Because their valuations only expanded modestly, that impressive 58% price gain was fundamentally justified by real earnings growth, not pure speculation.

The Pharma Rebound:

A 69% gain is nothing to sneeze at, and the data actually backs it up. Total cash flow almost doubled from ₹42,000 Cr to nearly ₹72,000 Cr. Even though their efficiency metrics look flat, the sheer scale of operational cash generated means these companies successfully translated their sales directly into owner’s cash. The ones that survived the brutal downturn of the past few years without taking on reckless debt have proven just how resilient they really are.

Sector Performance & Fundamentals (Apr 2022 – Apr 2026)

ITBEES (IT Services)

Price Change: -4.02%

ROCE: 15.97% (2022) ➡️ 14.45% (2026)

Total Sector CFO: ₹1,19,068 Cr ➡️ ₹1,52,813 Cr

Median P/E: 22.74 ➡️ 23.50

PHARMABEES (Pharma)

Price Change: +69.33%

ROCE: 10.67% (2022) ➡️ 10.35% (2026)

Total Sector CFO: ₹42,045 Cr ➡️ ₹71,809 Cr

Median P/E: 27.12 ➡️ 30.44

MODEFENCE (Defense/Eng)

Price Change: +24.17%

ROCE: 7.29% (2022) ➡️ 8.93% (2026)

Total Sector CFO: ₹38,598 Cr ➡️ ₹15,137 Cr

Median P/E: 31.35 ➡️ 56.09

BANKBEES (Banking)

Price Change: +57.78%

ROCE: 19.98% (2022) ➡️ 22.08% (2026)

Total Sector CFO: ₹2,76,677 Cr ➡️ ₹3,49,637 Cr

Median P/E: 10.29 ➡️ 14.24

FINIETF (Financials)

Price Change: +55.62%

ROCE: 61.20% (2022) ➡️ 80.13% (2026)

Total Sector CFO: Because of accounting quirk, operating cash flow are always -ve and is not great way to judge the sector

Median P/E: 15.79 ➡️ 19.28

The Bottom Line

At the end of the day, you don’t get paid for buying what is popular; you get paid for buying what is mispriced. The market might be a voting machine in the short run, but in the long run, it is a weighing machine—and sooner or later, it always weighs the cash.

Disclaimer: Do your own due diligence before investing.

Join the Hunt

The market is noisy. Your inbox shouldn’t be.

By subscribing to Budget Tiger, you’re making a commitment to rational, owner-oriented investing. Here is my commitment to you:

One email a week: Delivered every Sunday at 8 AM.

100% Signal: Deep research powered by AI, vetted by human judgment. No spam, no filler.

Always Free.

You’ll get one email a week from me. It will cover:

The Noise: What the AI hype-filter caught (and why to ignore it).

The Signal: The fundamental truth about the cash flows and moats.

The Verdict: A qualitative deep dive, not a quantitative score.

Leave the noise behind. Enter your email below to receive next week’s edition of Budget Tiger in your inbox.

Noteworthy.