What I learned from analyzing fragility of 2168 listed Indian companies / 106 Industries

Introduction:

Fragility is a term that describes how vulnerable a system or an asset is to external shocks or stressors. A fragile company is one that suffers large losses when market conditions change unexpectedly or unfavorably as against Robust/Antifragile companies which can withstand such changes/shocks. Similarly there is scope for large drawdowns if a portfolio comprises fragile companies.

I explained about concept of Fragility in detail and how to measure the same through my following posts

How to build an Antifragile Portfolio (budgetiger.in)

Methodology:

I shortlisted companies with market capitalisation of more than Rs 100 Crs and there are 2168 such listed companies in India. Smaller companies are a different segment as they are mostly localized companies wherein they generally have one or two customers. They generally have limited options due to which by default they are more fragile. Due to this, I excluded companies with market capitalisation of less than Rs 100 Crs.

I use the method of optionality for measuring fragility as explained in my various posts. As per the methodology, a company with more obligations and fewer options is more fragile as against a company with fewer obligations and more options. Less fragile companies are either Robust or Antifragile companies.

I measured fragility of each company based on following four parameters and using method of optionality:

Equity as a % of Balance Sheet Total - Higher the percentage indicates lower the obligations of a company

Break Even Sales as a % of Actual Sales - Lower the percentage indicates more the options available to a company

Return of Capital Employed - Higher the percentage indicates more the options available to a company

Cash Flow from operations / (Replacement Capex plus Yearly Debt Obligations) - Higher the ratio indicates lower the obligations of a company

Based on the above parameters, I arrived at a fragility score on a scale of 0 to 10 for each company wherein a score of 0 indicates least fragile company i.e. robust/ antifragile and a score of 10 indicates most fragile company.

I used the financials of FY22 for measuring the fragility of each company. FY22 is part of the disruptive 2 years COVID period wherein few industries were more impacted than others due to COVID. Accordingly, fragility scores for few companies/ industries are likely to change based on FY23 financials. A fragility score is dynamic and will change every quarter/year based on financials of a company. For example, if a debt free company takes a huge loan for a greenfield project, then fragility of the company will increase. Similarly a major dip in sales of a company will increase the fragility score of a company.

The universe of 2168 companies are further subdivided into 106 industries and I arrived at the average fragility score of each industry based on the fragility score of each company in the Industry.

The fragility score as calculated above only measures the fragility of a company without considering the entry valuation of an investor. Entry valuation for an investor is an added variable and if an investor invests in a robust/antifragile company at high entry valuation, then fragility at portfolio level increases.

Learnings

Low fragility scores indicate robust or antifragile companies/ industries. Higher the fragility score on a scale of 0 to 10 higher the fragility.

Least Fragile Industries

Following are the top 20 Industries with least fragility scores i.e. these industries are Robust or Antifragile.

Pharmaceuticals - Multinational companies panned out to be the least fragile industry with a fragility score of 1.73 i.e. the industry is very Robust/ Antifragile in nature. The industry comprises companies like Abbott India, Astrazenca Pharma, GSK, Novartis India, P&G Healthcare, Pifzer and Sanofi India each of which individually have very low fragility scores.

The other industries in top 5 i.e. least fragile are (in order of ranking):

Cigarettes - Godfrey Philips, VST, ITC;;

Personal Care - Mutlinational - Colgate-Palmolive, Gilette India, Hindustan Unilever; P&G Hygiene

Petrochemicals - A surprising entry in top 5 with small cap companies like Bhansali Engineering Polymers , Panama Petrochem Limited, Supreme Petrochemicals Limited, etc. Most of these companies had a very good performance during FY21 and FY22 which is possibly due to COVID disruption. We need to see how the scores of these companies will change with FY23 and later financials.

Pesticides / Agrochemicals - Multinational - There is only one company in this industry i.e. Bayer CropScience Limited. The Bayer group launched its Indian operations in 1958 by setting up an agrochemical manufacturing unit under BCSL. BCSL manufactures and markets crop protection solutions, and trades in seeds on behalf of Bayer Bioscience Pvt Ltd.

Most Fragile Industries

Following are the top 20 Industries with highest fragility scores i.e. these industries are more fragile than other industries.

I expected Banks and NBFCs to be the most fragile industries due to the nature of their business model. I explained this in detail in my post The Fall of SVB Bank, Signature Bank - What Makes Banks Fail? (budgetiger.in)

Accordingly top 6 Industries include Banks - Public Sector; Banks - Private Sector & Finance - Term Lending Institutions.

It is surprising that the most fragile Industry panned out to be Automobiles - LCVs/ HCVs with a fragility score of 7.74. The industry includes companies like Ashok Leyland, Force Motors, Tata Motors, SML Isuzu, Olectra Greentac. Most of these companies incurred losses during 2 years of COVID i.e. FY21 & FY22. These companies also are leveraged due to which the fragility score of these companies is high based on FY22 financials indicating that these companies are highly fragile. We need to see if the fragility score decreases based on FY23 financials for these companies.

The other 2 industries in top 6 are Telecommunications - Service Provider & Cables - Telephone.

Cables - Telephone comprises Sterlite Technologies; Birla Cables & Aksh Optifibre. All three companies are into manufacturing of Optical Fibre cables. I could not find any correlation of high fragility score with COVID. The high scores may be due to the capital intensive nature of the industry wherein the companies had to raise debt for capex outlay. It may also have to do with the fact that most of the projects executed by these companies are floated by Central and State Governments due to which these companies have limited pricing flexibility.

Telecommunications - Service Provider comprises Bharti-Airtel, MTNL, Reliance Communications, Tata Teleservices Maharashtra Limited, Netflinx, Onmoblie Global, Tata Communications, Tejas Networks, Vodafone Idea & Railtel Corporation. The high fragility scores may have to do with high regulatory intervention in the Industry and also intense competition in the Industry. Railtel Corporation & Tejas Networks are the least fragile companies within this industry with scores of 4.9 and 4.6 respectively. Railet Corporation is a PSU company and classified as Miniratna”. Tejas Networks Ltd is a global R&D-driven telecom equipment company headquartered in India. It designs, develops and manufactures high-performance optical and data networking products that are used by telecom service providers, utilities, government and defense networks. Ken had done detailed analysis of the company in its post The Tata wind beneath Tejas Networks’ wings carries investors away (the-ken.com)

Other Learnings:

There is scope for change in fragility scores for few industries as the analysis is done based on FY22 financials which is a COVID disruptive year.

Few industries have companies with a wide range of fragility scores. For example, Recreation/ Amusement Parks Industry has Imagica Entertainment with a fragility score of 8.6 vs Wonderla Holidays with a score of 2.92 and Nicco Parks with a score of 1.48. Imagica Entertainment alone increased the industry score due to which the Industry got a score of 4.35.

There is no correlation between valuation and fragility scores. I used P/E as a valuation parameter for this analysis. Below is the scatter plot between P/E and Fragility Scores

As we can observe, there are both low and high P/E companies with various fragility scores.

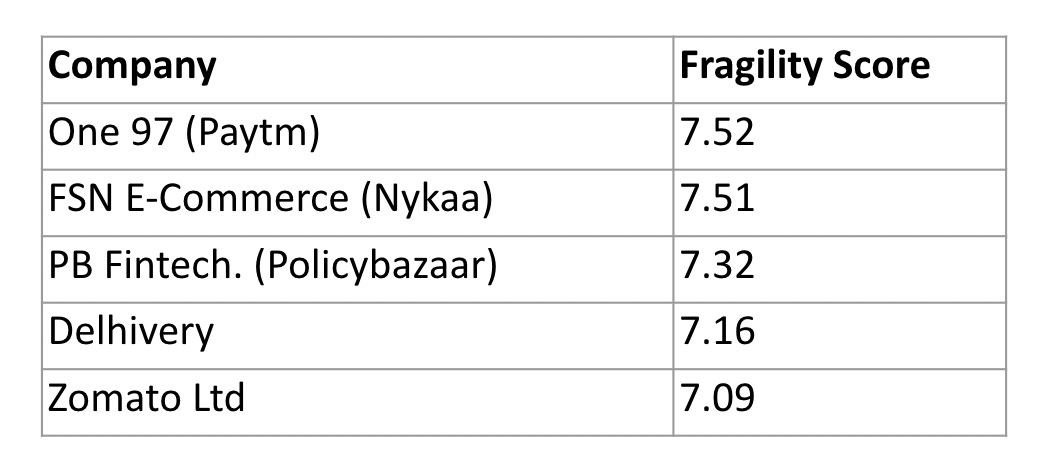

The fragility score of all 5 new age tech stocks is more than 7 indicating they are in the top 20% percentile of most fragile companies in the universe of 2168 stocks. All the 5 companies scored high fragility on ROCE, CFO/ (Replacement Capex + Yearly Debt Obligations and Breakeven sales as % of Actual Sales which is not surprising as all these companies are yet to turn cash flow positive. However all these companies scored very low fragility in terms of Equity as % of Balance Sheet Total as all these companies had very low Borrowings/ Debt and other liabilities.

If you want to learn more about how to use fundamental analysis for stock market investing, don’t miss out on my newsletter. Every Sunday, I’ll send you a post like this one with valuable insights. To subscribe, just enter your email below. And if you know anyone who might benefit from this newsletter, please share it with them too. Thank you for your support!

How about industries exposed to changes in regulations? Say an activist govt. could come in and ban cigarettes? Indian Pharma may find it hard to export due to reg pressure etc

Surprised not to see Chemical or Specialty Chemical industry not featuring in the High fragile industry.

Also would Reliance feature in Diversified Mega industry (Low fragility) or Petro Chemical / Refinery/ Telecom/ FMCG retail .... ??